The longer-term factors driving the housing market should make you highly optimistic about the segment right now, even if the near-term outlook is not as exciting.

On May 10, the Conference Board stated that real GDP growth should come in at 0.7% this year, dropping to 0.4% next year. Consumer spending continues to slow as a result of inflation, while business spending continues to slow because rate increases and labor market tightness are increasing costs for companies. Government spending, particularly on infrastructure, is a positive.

Another positive is the labor market, where the unemployment rate of 3.4% remains at historic lows. Job growth remains positive, with most of the additions in professional and business services, healthcare, leisure and hospitality, and social assistance. [BLS data]. A strong labor market means sustained consumption, as well as continued demand for housing.

Third, the Fed used encouraging language about future rate hikes, so many in the market thought that May would be the last one this time round. Although the Conference Board doesn’t consider it likely, stabilization in the interest rate will be positive for businesses, including for homebuilders. As a result, mortgage rates will also stabilize, helping home buyers.

Fourth, personal income continued to increase in March by 0.3%, led by private wages and salaries, receipts on assets and an increase in personal dividend income. A 0.1% reduction in spending allowed a personal saving rate of 5.1%. Savings help you make down payments.

All of this doesn’t mean that the high inflation, high interest rates, high mortgage rates and escalating home prices aren’t having a negative impact on the market right now. Along with the rising cost of land and materials and the shortage of skilled labour, which increases building costs, these factors are particularly hurting home affordability, which is telling in the data on first-time home buyers. The luxury segment is doing better than the rest.

According to Realtor.com data as reported by CNN, 15.6 million new households were formed between 2012 and 2022, and only 8.5 million single-family homes and 3.4 million multi-family units completed. This has created a huge shortage of available homes.

Plus, the population continues to increase, with an increasing number of people starting their families every year. This further increases the gap between demand and supply. Since many people have refinanced their homes in the last few years to take advantage of lower mortgage rates, they are unwilling to sell and move up because of today’s higher rates. Although this is the existing home segment, it affects the overall supply in the market with a corresponding effect on prices.

It will take several years for the market imbalance to correct itself and for prices to come down. Therefore, the high demand, strong pricing environment is likely to continue, making the segment a good long-term play.

Now turning to stocks, it’s worth mentioning that analysts expect most companies to report revenue and earnings declines this year, as the high prices continue to keep some buyers out and other factors of production (discussed above) increase costs. But it’s likely to be a temporary phenomenon as the US battles with a possible recession, however soft it may be. Analysts are equally optimistic that things will change next year, when growth returns:

MDC Holdings, Inc. (MDC)

Zacks #1 (Strong Buy)-ranked MDC is expected to report a revenue decline of 30.2% and earnings decline of 57.9% in 2023, followed by a revenue increase of 5.0% and earnings increase of 20.8% in the following year. The 2023 estimate has increased 69 cents (27.2%) in the last 30 days while the 2024 estimate increased 91 cents (30.4%), as analysts revised estimates.

DR Horton, Inc. (DHI)

This Zacks Rank #1 stock is expected to report revenue and earnings declines of 3.6% and 33.3% this year, returning to growth with +1.1% in revenues and +6.4% earnings next year. But if recent estimate revisions are an indication of any trend, the company may ultimately generate growth this year as well: the 2023 (ending September) estimate is up $1.93 (21.3%) and the 2024 estimate is up $2.15 (22.5%) in the last 30 days.

Taylor Morrison Home Corporation (TMHC)

The Zacks Rank #1 stock is expected to report revenue and earnings declines of 14.4% and 27.3%, respectively. In 2024, they’re expected to grow 7.4% and 6.7%, respectively. The 2023 estimate is up 34 cents (5.3%) while the 2024 estimate is up 22 cents (3.1%) in the last 30 days.

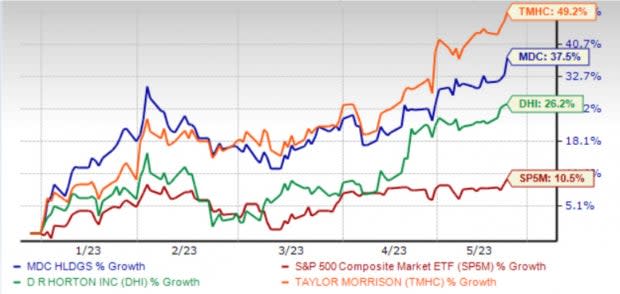

Price Performance Year-to-Date

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download the 7 Best Stocks for the Next 30 Days. Click to get this free report

DR Horton, Inc. (DHI) : Free Stock Analysis Report

MDC Holdings, Inc. (MDC) : Free Stock Analysis Report

Taylor Morrison Home Corporation (TMHC): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research